The recent struggles of former talk show host Wendy Williams have brought significant attention to the complexities and potential pitfalls of guardianship arrangements.

Widows and Widowers’ Estate Plans Amended

The loss of a spouse can be extremely challenging emotionally, financially, and spiritually. An aging widow or widower may find herself in a complex financial situation with more questions than answers as one spouse handles family tax and estate planning. It is a mistake to think that one’s estate plan is complete after the death of a spouse. Many times, there are decisions to make and act on within a set timeframe. Reviewing and reassessing your finances and estate plan should be a top priority.

Start by taking an inventory of your current bills; making a plan that covers those expenses for the next six to twelve months. If your spouse’s social security monthly benefit is higher than yours and your marriage was ten years or more, petition to receive the higher dollar amount. Put off making big decisions if at all possible, during this time. Adapting to the loss of a loved one can cloud good decision-making and allowing for time to analyze decisions may even find you developing new financial goals. However, identify and act on those decisions with deadlines, particularly the portability election on the decedent’s estate tax return and any probate timelines. Be particularly careful during tax time and work closely with your tax preparer to understand both your deceased spouse and your taxes. It is not uncommon for a widow to discover previously unknown accounts.

If you have a solid relationship with your family attorney and financial advisor, reach out to them for guidance. These professionals are well versed in the processes that accompany the loss of a spouse. If you are not familiar with these individuals, make appointments to meet with and review your current situation. Ask for strategic options and see how they fit into what may become your forward plans. Re-evaluate your investments and match needs to risk tolerance. Many widows are happy with a lesser return if stability is the offset. Be sure you are content with your investment philosophy before making significant changes, carefully weighing professional input.

Keep your formal estate plan updated. Laws change, and so has your situation. Ensure that all beneficiaries on IRAs, life insurance, and some investment accounts reflect your current wishes. If necessary, update your power of attorney for both financial and medical directives. When outright gifting to your children, remember it may create problems if there were to be a later divorce. An ex-spouse can lay claim to the gifted property, which you can lose in a lawsuit. Speak with your estate planning attorney as trusts are a beneficial entity to manage and protect the property of significant value. Trusts are also worth considering protecting substantial assets that do not have a beneficiary designation to bypass probate and protect your heirs.

Take stock in your home, weighing your financial situation and your emotional connection to your home. Does it make sense to stay in your current residence? Is it financially possible to do so? Even if the home is mortgage-free, maintenance and upkeep of the home and property can become overwhelming and expensive. Alternatively, many widows prefer to remain in the home with longstanding memories of their spouse and children growing up in the environment. Even though it may make economic sense to move, the emotional ties to the property may be in the best interest of the widow to preserve.

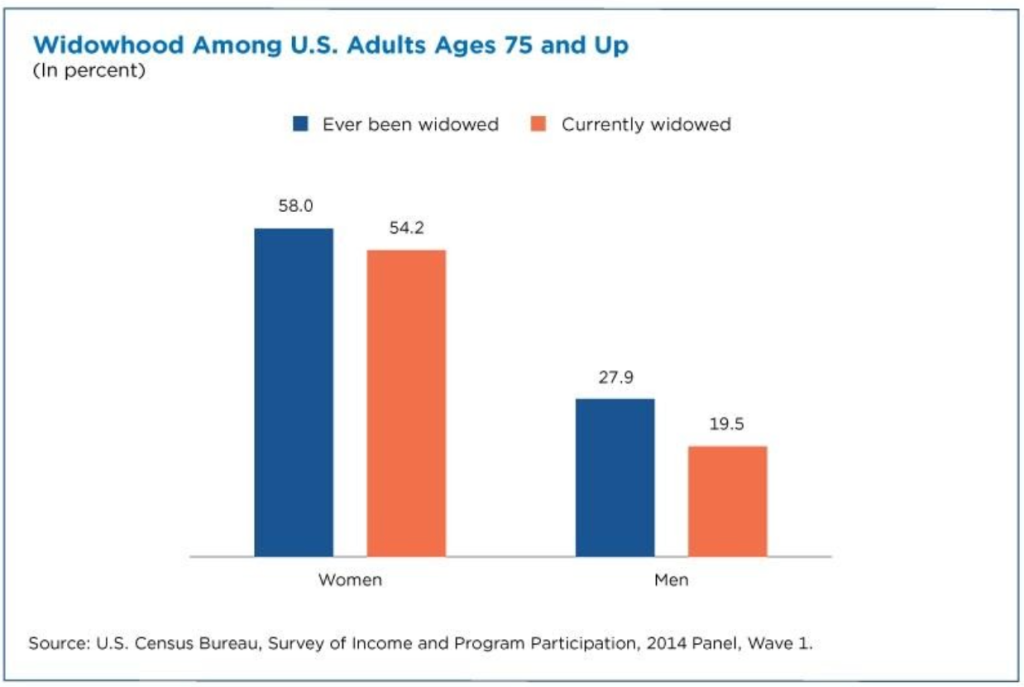

According to a Fidelity Investments survey, most Americans who find themselves widowed are female, and nearly seventy percent will retain a new financial advisor within the first year of the death of their spouse. Regardless of why this happens, it is clear that amending financial goals and revisiting the estate plan is likely to be the actions of a widow. Predictions are that women will inherit close to thirty trillion dollars of intergenerational wealth transfers over the next few decades. Becoming educated about family financial decisions for all widows(ers) is of the utmost importance, particularly for women who tend to outlive their husbands.

How a spouse passes, whether from a lengthy disease battle or taken quickly, matters not. The grief is still there. How long and deep the grief varies significantly among individuals. While it is essential to address time-sensitive decisions, it is best to make significant financial changes when a widow feels emotionally intense and clear-minded to avoid making regretful decisions. Professional guidance and advice are of the utmost importance to fully understand your situation and the decisions you need to make. While the process can be complex, even heart wrenching, it is of utmost importance to your future to handle what is before you competently. Please contact our Houston office at 713-582-5088.